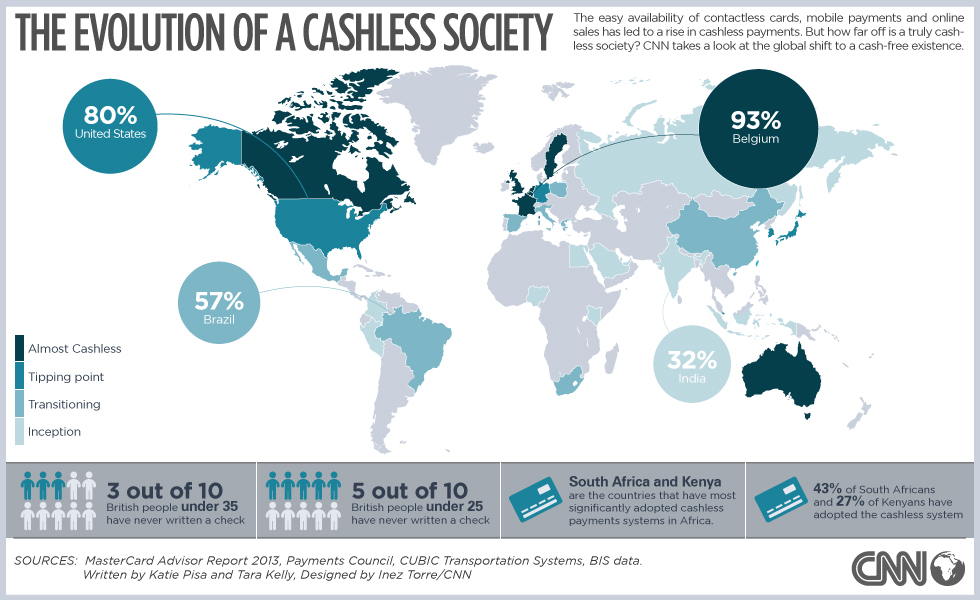

Here are the front-runners: the first percentage figure is for the non-cash payments' share of total of consumer payments; the second is the percentage of the population who have a debit card. These statistics (which date from April 2015) come from www.letstalkpayments.com

Belgium: 93%/ 86%

France: 92%/ 69%

Canada: 90%/ 88%

UK: 89%/ 88%

Sweden: 89%/ 96%

Australia: 86%/79%

The Netherlands: 85%/ 98%

This is a useful up-to-date glbal summary: 'Around the World in 80 Payments: global moves to a cashless economy' [The Conversation.com/Jan 2016]

To understand the complexities and implications of this move away from hard cash, this post concentrates on what is happening in Sweden which has been the topic of a wide variety of journalism over recent months. Its a interesting story.

*

Sweden was the first European country to implement paper money (1661) and is now amongst the first to try and eliminate it. The sign "Vi hanterar ej kontanter" ("We don't accept cash"). is everywhere. Even the homeless sellers of street newspapers now carry mobile card readers and church collections are paid by contactless cards. When there was a spate of attacks on bus drivers for their fare, Stockholm banned cash on public transport. Apparently one of the only areas where you still need cash is to purchase illegal drugs.

Between 2010 and 2012 alone, more than 500 branches of the six largest Nordic banks have gone cash free and, in that same period, 900 cash machines were removed. (Sweden installed its first ATM machine in 1967, two years before the U.S). Supermarket check-outs are now one of the last places where cash can be obtained.

According to Niklas Arvidsson, a professor at Sweden's KTH Royal Institute of Technology and author of "The Cashless Society", the advantage to the banks of this move is that they can eliminate bank robberies, theft and dirty money, which chimes in with a government crackdown on crime and terrorists.

"At the offices which do handle banknotes and coins, the customer must explain where the cash comes from, according to the regulations aimed at money laundering and terrorist financing," he says. Bank staff are required to file police reports in response to suspicious cash transactions.

In addition, if all payments are digital then the bank can monitor exactly how much money each customer spends where on what.

Conducting commerce with cash costs both banks and business money. It is certainly in the interest of banks to price cash out of the market as they are and will earn substantial income through card and electronic payments.

In a country where bank cards are routinely used for even the smallest purchases, there are less than 80 billion Swedish crowns in circulation (about EUR8 billion), a sharp decline from 2009's figure of 106 billion. Only some 40 and 60 percent is actually in regular circulation.

Arvidsson explains that his fellow citizens have a relaxed attitude towards these drastic changes for three basic reasons: firstly most Scandinavians have not carried any cash or been to a bank in years; secondly the Swedes appear to have a much higher level of trust when it comes to the handling of their personal data by banks or their government; thirdly, they have enthusiastically embraced digital technology.

Sweden is the first country in which every child gets a government-issued iPad on the first day of school and they learn to write on a keyboard and not by hand. Children's pocket money is transferred to their bank account.

Also Sweden is approaching an environment of negative interest rates, which puts pressure on customers, in the form of higher bank charges or fees, to spend their money. Eriksson says "I've heard of people keeping cash in their microwaves because banks won't accept it."

"There is also a demographic development behind this," says Arvidsson."Younger people do not start using cash but instead move directly into new services, while older people—who are the most frequent users of cash—reduce their spending as they get older and older."

Sweden could get close to eliminating cash in 8 or 10 years although Arvidsson believes that a change in the law to make cash no longer legal tender will not happen until around 2040.

New Swedish notes and coins have recently been introduced.

According to Helen Russell in The Guardian:

The country’s highest-profile cash-free campaigner is Abba’s Björn Ulvaeus. After his son was robbed several years ago, Ulvaeus became an evangelist for the electronic payment movement, claiming that cash was the primary cause of crime and that “all activity in the black economy requires cash”.

The man who composed 'Money, Money, Money' has been living cash-free for more than a year and says the only thing he misses is “a coin to borrow a trolley at the supermarket”. Abba the Museum has operated cash-free since opening in May 2013 and Ulvaeus says Sweden “could and should be the first cashless society in the world”.

The drive to a cashless society is supported by the UN Capital Development Fund’s Better Than Cash Alliance which aims to accelerate the shift to electronic payments, funded by the Bill & Melinda Gates Foundation, MasterCard and Visa among others.

*

How much boosterism there is in the above narrative must be questioned in the light of info from business website Quartz. They claim that:

'...data from the European Central Bank indicate that Swedes, while enthusiastic about bank cards and digital payments, still regularly withdraw quite a bit of money from ATMs. Surveys from the Riksbank show that for transactions under 100 kronor, 41% of people still prefer to use cash.'

Helen Russell reports: “A recent survey I worked on showed that two-thirds of Swedes think carrying cash is a human right,” says Arvidsson. “We like having our own currency and it fits in with the identity of being a Swede; we’re even releasing new banknotes in 2015. So people like to know their cash is there, even if they don’t necessarily use it.”

She also highlights another issue: 'The digital payment revolution is also a challenge for tourists, who need pre-paid tickets or a mobile registered in Sweden to catch a bus in the capital. Many have also endured mild chaos at the one of the country’s first cashless festivals this summer when the payment system broke down and people ended up resorting to old-fashioned IOUs.'

Not everyone is convinced of the idea. Björn Eriksson, a former police chief and head of Interpol, who now heads a lobbying group for the security industry, takes the view that this is just a money-making plot by the banks. He points out there may have been a dramatic fall in bank robberies but this is matched by a steep rise in cybercrime.

According to figures from Sweden's Ministry of Justice quoted in The Guardian, in 2014 there were 140,000 electronic fraud cases, almost double the amount ten years ago.

*

'Sweden gets closer to being the first cashless society with negative interest rates' by Jim Edward [October 2015/UK Business Insider]

'Sweden is on track to becoming the first cashless nation' [October 2015/Phys.org]

'Will Sweden be the first country to get rid of cash' [fastcoexist.com]

'Sweden is on its way to becoming the first cashless society on earth' by Amy X. Wang [Quartz/October 2015]

'Welcome to Sweden - the most cash-free society on the planet' by Helen Russell [The Guardian 12th November 2014]

'In Sweden where even banks shun cash' by Liz Alderman [ International New York Times/28 Dec 2015]

*

PS: Christopher Mimms in the MIT Technology Review (Feb 2012) on 'The End of Money' by Wired contributing editor David Wolman:

[It's] 'ostensibly about the twilight of cash and its replacement with a panoply of more efficient means of exchange. (Think transfers via NFC on smartphones and biometric wallets.) But Wolman is such a thorough reporter of the subject that it’s possible to finish his (excellent, highly readable) book and come away with a conclusion opposite his own.'

He concludes: 'The problem with all of the arguments for a cashless society is that they’re rational, and our attachment to cash is not. This might be less true in nations that have already given up their national currency to become part of a regional currency block (the EU, and countries like El Salvador that have adopted the dollar as a national currency), but as long as there are financial superpowers whose paper money is covered with what amounts to propaganda for the strength of their central banks, cash is here to stay.'

*

BITCOIN

If, like me, you have found it hard to get your head around the nature and purpose of Bitcoin you may find this piece in The Economist useful. It begins:

'Unlike traditional currencies, which are issued by central banks, Bitcoin has no central monetary authority. Instead it is underpinned by a peer-to-peer computer network made up of its users’ machines, akin to the networks that underpin BitTorrent, a file-sharing system, and Skype, an audio, video and chat service. Bitcoins are mathematically generated as the computers in this network execute difficult number-crunching tasks, a procedure known as Bitcoin “mining”. The mathematics of the Bitcoin system were set up so that it becomes progressively more difficult to “mine” Bitcoins over time, and the total number that can ever be mined is limited to around 21m. There is therefore no way for a central bank to issue a flood of new Bitcoins and devalue those already in circulation.'

More basic information on this Bitcoin site: https://bitcoin.org/en/you-need-to-know

In a major story (Jan 14th 2016) New York Times journalist Nathaniel Popper reveals that 'a nasty fight has torn apart the small brotherhood of Bitcoin developers and raised questions about the survival of the virtual currency.'

A more recent story in Newsweek (22nd Jan 2016) by Nicolas Cary 'Bitcoin: Too Big To Fail':

'The death of bitcoin has been proclaimed once again. Prominent developer Mike Hearn’s recent comments that the bitcoin experiment was over mark the 89th time the digital currency has been pronounced dead since it first launched in 2009, at least according to one website dedicated to tracking bitcoin obituaries. While it’s sad to see a talented programmer like Hearn turn his back on bitcoin, there are still thousands of people working on making the world’s first digital currency a success.

'The bitcoin network has been running without interruption for seven years now; a feat no banking system can claim. Bitcoin and its underlying blockchain technology—an online ledger that records every bitcoin transaction—represent a fundamental innovation that can dramatically speed up transaction times.'

Published today: Big Miners Back Bitcoin Classic As Scaling Debate Evolves

No comments:

Post a Comment